Are you looking to buy your first home, and not sure where to start? We can help you identify what first time home buyer programs in Colorado may be best suited for you.

The information provided on this page is geared for first time buyers who may not qualify for conventional financing. This includes various borrowers, such as those who are self employed, people with bad credit, and/or borrowers with low income. If you fit one of these scenarios, or any combination of them, you may need to seek out a non-prime mortgage, FHA loan, or USDA loan.

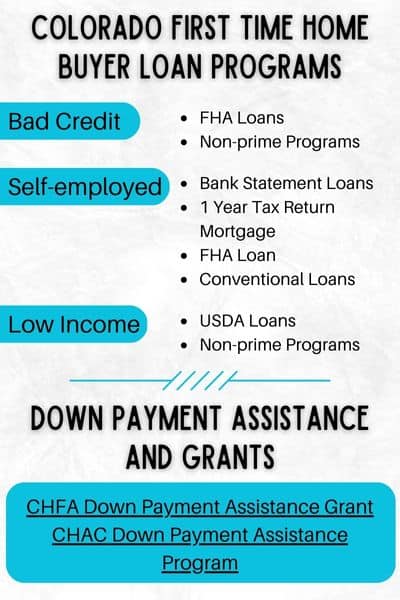

Colorado First Time Home Buyer Loan Programs

Below are some of the top non-prime loan programs for first time home buyers in Colorado. If you have any questions, or would like to see which programs you qualify for, contact us for a free consultation.

Bad Credit – Colorado First Time Home Buyer Loans

Whatever the reason is that you have bad credit, you still may be able to qualify to get a mortgage. There are loan programs that allow credit scores as low as 500, and without any waiting periods for major credit events (such as a recent bankruptcy, foreclosure, or short sale).

- FHA Loans – If your credit is somewhere between a 500-620, you should first see if you are eligible for an FHA loan. This is especially the case if your credit is between a 580-620, since with a 580 score or higher you may get approved for a down payment of only 3.5%. If your credit is between a 500-579, you may still be able to get an FHA loan, but a 10% down payment would be required. You can learn more about FHA loans, and also view some of the best FHA lenders in Colorado, on this page.

- Non-Prime Programs – There is a fairly large selection of non-prime loan programs available to home buyers with bad credit. Some of these loan products allow credit scores all the way down to 500, but usually will require at least a 10-20% down payment. One of the major advantages of the non-prime programs our lenders offer is that you can still qualify for a home loan even just 1 day after a bankruptcy, foreclosure, or short sale. These loan products also often will allow higher DTI ratios (debt-to-income ratios) than conventional and FHA loans.

You can learn more about the top bad credit mortgages, or if you have any questions, or want to see what programs you are eligible for, get in touch with us today.

Self Employed – Colorado First Time Home Buyer Loans

There are several different home loan programs available to self-employed borrowers. We can assist you in determining which lender and program may be best suited for you. If you provide us with some information, including your estimated credit, desired loan amount, length of self employment, location, and your contact details, we can match you with who we think will be the best lender for your home loan. Simply fill out this form, and we will connect you with a lender offering self employed mortgages.

- Bank Statement Loans – Self employed borrowers have the option to qualify for a mortgage without using any tax returns at all, but instead using 12-24 months worth of bank statements to prove income.

- 1 Year Tax Return Mortgage – Are you newly self employed? A 1 year tax return mortgage could be the perfect loan option for you. Instead of having to provide 2 years worth of tax returns, you only need to provide a tax return for 1 year. You can learn more about these programs, on this page.

- FHA Loans – Many people wrongly assume that FHA loans are not available for the self-employed. It is true that applications of self-employed borrowers are more closely looked at, but it is still feasible to get an FHA loan when self-employed.

- Conventional Loans – Being self-employed does not automatically disqualify you from obtaining a conventional loan. Similarly to FHA loans, conventional loans require self-employed applicants to be more closely reviewed. Underwriters will scrutinize the stability of your employment and income to determine if it is reliable enough to approve your application.

We can help answer all of your questions, and also see you see what loan programs you may qualify for. If you would like some help, get in touch with us today. You may also learn more about self employed mortgages to see what options may exist for you.

Low Income – Colorado First Time Home Buyer Loans

If you have low income, but have stable employment, you may be able to get a home loan. In fact, some mortgages, such as USDA loans, are specifically available to people with lower income.

- USDA Loans – The USDA rural development loan is intended for lower income households. In fact, you can not get a USDA loan unless your income is less than 115% of the median average income of the county that the property is located in. If you would like, you can view the USDA income limits, which are set at the county level. If you have really low income, you may qualify for a special USDA loan, known as the USDA direct loan, which is geared for the lowest income borrowers.

- Non-Prime Programs – One of the main obstacles in obtaining a mortgage with low income is meeting the DTI ratio requirements. It is not so much how much money you make total, but what percent of your income your monthly debts are compared to your income (monthly debts including your monthly mortgage payment and other credit reported debts, such as credit cards and car payments). Conventional loans have a maximum DTI ratio of 43% (unless you have high income or excellent credit). For FHA loans, the max DTI ratio is also 43%. Fortunately, there are non-prime loan products that allow higher DTI ratios.

We would be glad to answer all of your questions about low income mortgages for first time buyers, or if you want to be matched with a non-prime lender, get in touch with us today.

Colorado First Time Home Buyer Down Payment Assistance and Grants

There are many down payment assistance programs offered in Colorado. In fact, there are so many, that we are only including the top two options. A lot of down payment assistance programs are provided locally, such as through a city or county. If you would like some help, we can assist you in seeing what down payment assistance programs you qualify for.

- CHFA DPA Grant – The Colorado Housing and Finance Authority offers a down payment assistance grant to first time home buyers in Colorado. How the grant works, is you can receive up to 4% of the purchase price, which does not have to be repaid! So if you buy a home for $300,000, you would receive $12,000 in assistance that could be used for your down payment and closing costs. In order to qualify, you must meet certain income limits, and must have at least a 620 credit score. The grant is only eligible to be used with an FHA or conventional loan, however. It can not be used with any special non-prime loan products.

- CHAC DPA Program – The Colorado Housing Assistance Corporation offers first time buyers a down payment assistance program that offers up to $10,000 in assistance. The assistance comes in the form of a loan (acting as a second mortgage with a lien on the property). To qualify for the assistance, you must complete a first time home buyer class, and meet certain income limits (which is 80% of the average monthly income for all locations in Colorado, except Arvada, where you can have up to 100% of the average monthly income).

The above two down payment assistance programs are just the two largest available in Colorado. There are many other programs that exist, which you may be eligible for. Would you like to find out what assistance you may be eligible for? We can help you get connected with a lender based on your location, who can assist you.

Other Colorado First Time Home Buyer Down Payment Assistance Programs

These are some additional down payment assistance programs in Colorado. You will need to apply for them and get approved. However, they will ask you to get pre-approved by a lender first. That is where we can help if you can just complete this short pre-approval request form.

Metro Mortgage Assistance Plus Program

Colorado First Time Home Buyers with Bad Credit

For Colorado residents with bad credit, you can still purchase a home as a first time home buyer. FHA guidelines permit credit scores as low as 500 in Colorado. However, the down payment will be 10% if your credit scores are between 500-579.

Although you can get a mortgage as a first time home buyer with bad credit, qualifying for the assistance programs may be more challenging. Many of the Colorado down payment assistance programs do have minimum credit score requirements. Your first step is to get pre approved for a mortgage based upon your income and debt. Then, you can take the pre-approval and bring it to the down payment assistance program to see whether you qualify with your credit scores.

Colorado First Time Home Buyer Income Limits

When applying for a mortgage as a first time home buyer in Colorado, there will not be any income limits if you are applying for an FHA loan. However, USDA loans do have income limits.

The down payment assistance programs in Colorado may have income limits. The purpose of having the limits is to prevent individuals who make a lot of money from using down payment assistance when those with lower income may need the funds more.

We Are Here to Help

We understand that buying your first home can be intimidating and even a bit puzzling. We are available to answer your questions, and help you find the best Colorado mortgage lender and loan program for your unique situation. You can browse through our website to learn more about different loan programs, or contact us for a free consultation.