What Credit Score Do You Need to Buy a House in 2024?

Many assume that you need to have good or excellent credit to buy a house. This is definitely not the case, especially in 2024 where there are now many mortgage programs for borrowers with bad credit. Even if you are a first time home buyer, you may be able to get a mortgage with a low credit score. In fact, both FHA loans and non-prime loans allow a borrower to get a mortgage with a credit score as low as 500!

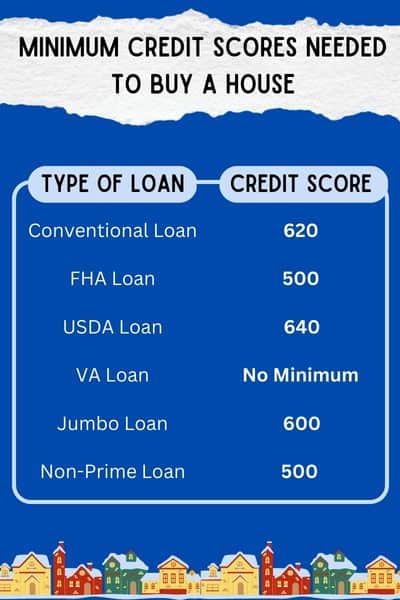

You can view the minimum credit scores needed for the most common types of mortgages below.

Minimum Credit Scores Needed to Buy a House

Below are the minimum credit score requirements for conventional, FHA, VA, USDA, jumbo, and non-prime loans. If you are not sure what type of home loan is right for you, and would like some help, we can have a lender contact you. To request a free consultation from a mortgage lender, fill out this form.

Credit Score Needed for a Conventional Loan – 620 or higher.

In some cases, lower credit scores are approved, if there are sufficient “compensating factors”. Most applicants will need a credit score of at least 620 to be approved though.

Credit Score Needed for an FHA Loan – 500 or higher

FHA loans only require a 500 minimum credit score. However, to be eligible for a 3.5% down payment, you must have a credit score of 580 or higher. If your credit is between 500-579, you may still get approved for an FHA loan, but will be required to put 10% down.

Credit Score Needed for a USDA Loan – 640 or higher

In order to get an automated approval, you need a 640 credit score or higher. However, lower credit scores can still be approved through manual underwriting, if your overall application is satisfactory.

Credit Score needed for a VA Loan – No minimum credit score required.

There technically isn’t a minimum credit score requirement for VA loans, but the majority of VA lenders want to see at least a 620 credit score. If you are a veteran or active duty military member, and your credit score is below a 620, we encourage you to still see if you can get approved.

Credit Score Needed for a Jumbo Loan – 600 or higher

Most jumbo lenders require a borrower to have a credit score of 720 or higher, but there are some non-prime jumbo lenders that offer programs to borrowers with credit scores as low as 600.

Credit Score Needed for a Non-Prime Loan – 500 or higher (or no minimum score required)

Non-prime lenders usually either have a minimum credit score requirement around 500, or no minimum credit score requirement at all.

The absolute LOWEST credit score needed to buy a house is 500. If you have scores lower than 500, you may need to find a private money lender who is not so concerned about credit scores.

Best Credit Score to Buy a House

The best credit score to buy a house is a score over 750. Lenders offer better rates for higher credit scores which means the higher the score, the better your rate will be. If your rate is lower, then your monthly payment will also be lower. A higher credit score and lower rate may also help you to qualify for a larger purchase price.

It may take some time to improve your scores and if you want until you are applying for a mortgage, it may be too late. If you have lower scores and wish to get approved for a mortgage, it can still be done with credit scores as low as 500.

What Does Your Credit Look Like?

The first step in the process of buying a home is knowing what your credit looks like. Mortgage lenders look at more than just your credit scores. They want to see your credit history, including what credit accounts you currently have, and if you have had any major derogatory marks, such as a bankruptcy or foreclosure.

Your credit report is actually one of the most important aspects of your mortgage application that will be looked at. Mortgage lenders have specific guidelines related to credit, including minimum credit score requirements. Your credit will not only influence the decision of whether or not you are approved, but also what interest rate you receive.

Would you like to pull a fresh credit report? All Americans are entitled to at least one free credit report each year through this website: Annual Credit Report.

The best way to understand what mortgage options may exist to you is speak with a mortgage lender. If you would like some assistance finding a mortgage lender, we can help match you with a lender in your location.

Click here to get matched with a mortgage lender

What is Considered a Good Credit Score?

There are different opinions and definitions of what constitutes a good credit score. Generally, good credit is considered anything above a 680. Some would say good credit is anything above a 700, or even a 720, but with a 680+ score, a borrower should expect to be awarded with a better interest rate.

Generally, the higher your credit score, the better the interest rate you will be offered. Fortunately, you do not need a 680 or higher score to get approved for a mortgage though.

Compensating Factors for Low Credit Scores

If you have lower credit scores than what is generally accepted for a mortgage program, you may still be able to get an exception if you have adequate “compensating factors”. Any of the following may be considered a compensating factor.

Long job history– If you have been on the same job, or at least in the same line of work for a lengthy period of time, this could potentially compensate for having a low credit score. If your income has been increasing or looks promising to increase, this could also be considered a compensating factor.

Larger down payment – One of the strongest compensating factors is to make a larger down payment. Borrowers who put more money down, or have plenty of equity, are much less likely to let a financed property foreclose. A larger down payment would be considered anything above 10%.

Cash reserves / savings – If you will have a decent amount of cash reserves left over after closing, this is a good compensating factor. Having money in savings increases the odds of you being able to repay your home loan, even in the event of temporary job loss.

Low debt – If you have low non-housing debt, such as credit cards, car payments, or personal loans, this may help your case. The lower your debt-to-income ratio, the more likely you may be able to get approved for a home loan, even with a credit score that does not meet the standard guidelines.

Additional income – If you have additional income that is not used in your qualifying debt-to-income ratios, but will contribute to your ability to pay your mortgage, this extra income help strengthen your chances of being approved.

When you apply for a mortgage with compensating factors, you give yourself the best chance for getting approved.

How to Improve Your Credit

There are many steps you can take to improve your credit.

Pay down credit card balances – One of the fastest and most effective ways of boosting your credit scores is to pay down credit card balances. The lower your credit card balances are in comparison to their credit limits,

Challenge errors – If you see any errors that are being reported, you should challenge the creditor. If you can prove that there is a mistake, you can possibly have the derogatory mark removed from your credit report.

Pay for derogatory items to be deleted – Another effective method of improving your credit is to negotiate with creditors to completely delete a derogatory item from your credit report. Some creditors and collection agencies refuse to delete the item even if you pay it in full. Be sure to clarify precisely what can be negotiated.

If you pay an old collection off, and it is not removed, it can sometimes actually have a negative impact on your credit (since an old derogatory mark will be updated, and start the clock over before it will be removed). Derogatory marks automatically drop off after 7 years, so if you can not have it completely removed, you may just want to wait for it to drop off on it’s own. This is especially the case if it is already a few years old. You can learn more about how to remove derogatory marks from your credit.

Open new credit cards – It is important to have at least 3 active credit accounts (trade-lines) present on your credit report. If you do not have 3 open accounts, such as credit cards, you may consider opening new credit cards. It is very important that you do not run the balances up though. You want to keep the balance of each card below 30%, and pay it off each month.

Having credit cards with high balances will hurt your credit. Also, the more debt you have, the higher your debt-to-income ratios will be, which can hurt your chances of being approved. So it is a balancing act of having adequate credit history, but without too much debt. Also, keep in mind that mortgage lenders usually want to see 12 months history with any credit account, so this would be more of a long-term strategy for improving your credit (for a future home purchase).

Get added as an authorized user – Another method that can be used to improve your credit rating is to be added as an authorized user to someone else’s credit card. You would want to be sure to only be added on a card where the primary user is responsible about keeping balances low, and paying every payment on time.

FAQ – Credit Score Needed to Buy a House

Can I Get a Mortgage with a Derogatory Mark?

It is absolutely possible to get a mortgage with a derogatory mark. There are many factors that come into play which will help determine whether the derogatory mark can stay, or whether it must be removed. It will come down to how the rest of your application shapes up. Whether you have high income, good credit other than the derogatory mark, a high down payment, etc.

My Credit Score is 700, can I buy a house?

A 700 credit score will help you to purchase a house but other factors will be weighed. Everything from your debt to income ratio, to your job history, and whether you have a recent bankruptcy. The bottom line is a credit score of 700 is very good and that alone will not prevent you from buying a house.

How Many Years of Credit to Buy a House?

You do not need to have many years of credit established to buy a house. Lenders can use non traditional credit such as phone bills, utility bills, and rent payment history to verify your credit worthiness so you can buy a house.

What Credit Score is Needed to Buy a House with No Money Down?

If you have no money down, then you are likely going to need a USDA loan. Most lenders are looking for credit scores of at least 580 for a no money down USDA loan.

Get Pre-Approved for a Mortgage

Would you like to see if you can get approved for a home loan? It is very easy to see what you can qualify for. Based on your location, and estimated credit, we will connect you with who we believe to be the best mortgage lender for you. You can expect to be contacted by a loan representative from the chosen mortgage lender within 1-2 business days.